You’ve just taken a step closer to becoming a homeowner. Here are some tips to help you get even closer to realizing your dream.

Pros and cons of taking a home loan in your youth

Pros of taking a home loan in your youth

Time factor: when you’re still young, you can take the loan for the maximum term. That means lower monthly payments.

Flexibility: your monthly income may be lower now than 10 years from now. With a lower income, you’ll probably be looking to keep your monthly payments as low as possible. As your earnings go up, you can always change the terms of the loan agreement.

Peace of mind: owning a home means no landlord will drop the news that they’re selling, and you’ll have to look for a new place. When paying rent, you’re probably paying for someone else’s loan, but with your own home loan, you are paying for your own home.

Investment into real estate: although a home loan is a big expense and a long-term obligation, you're really investing in your future.

Fixed amounts: there’s no risk of a landlord suddenly raising rent on you. The Euribor reference rate is variable and loan payments may change but you can change the terms of your agreement with us at any time – for example, extend the loan period and reduce the size of your monthly payments.

Freedom: you can turn your flat into the home you want to have. A home that looks like you.

Cons of taking a home loan in your youth

Loan-related costs: taking a loan is more than just making the down payment. You’ll have to pay for a property appraisal, the reservation fee, notary fees, signing fee and home insurance premium. The extras can add up to thousands of euros.

Long-term obligation: home loans are usually for 15–30 years. That can put a crimp into your other plans like travel, larger purchases or tuition costs.

Repair and maintenance costs: as a homeowner, you’re responsible for costs of upkeep of an apartment or a house. We recommend making sure that your insurance policy also covers liability insurance, protecting you from claims from third parties.

Less flexibility: homeownership ties you to a location. It’s harder to set off for a long tour of Asia or move to a new town.

Interest costs: over the loan period, you’ll be paying a significant amount in interest, especially in the first few years when you’re mainly paying off the interest.

Recommendations for saving toward your down payment

The earlier you start saving, the faster you’ll have the amount in hand. The earlier you take a home loan, the more flexible the terms we can offer. For example, you can set aside 10 euros every month. As your income grows, you will find that you are already in the habit of saving and you can set more aside.

Do you feel the 2% interest rate is insignificant and that you have the appetite for risk? You can reach your goal of saving faster with the Growth Account – money tends to grow faster when investing than by saving. When you sign a home loan agreement at LHV, we waive the service fee for selling assets on your Growth Account.

What if your own income isn’t enough to get approved for a loan?

KredEx

If you’re 35 or younger specialist in your field, we can offer you a home loan secured by KredEx for a lower down payment (as little as 10%). Visit the KredEx website to read about the details.

Get a parent to co-sign

It’s possible that your income will not be enough to borrow the amount you’d like. Besides surety from KredEx, you can also ask your parent to co-sign, which will give you more financial flexibility and increase your chances of being able to buy the home of your dreams.

Read more

How should I choose a home loan provider?

It might seem logical to base your decision on whoever has the lowest interest rate, we recommend also considering a few other factors.

Additional costs of borrowing

Besides interest rate, signing fee and home insurance cost also depend on the lender. Since all the extra costs can add up to thousands of euros (along with expenses that don’t depend on the lender, such as property appraisal, reservation fee and notary fee), it’s worth saving wherever you can and comparing these costs across different lenders.Fees for changes to loan agreement

Be sure to find out how much it will cost to amend your loan agreement at a certain lender. At LHV, fees for changes start at 100 euros.Early repayment charge

Will your lender dock you if you should want to repay the home loan earlier than the end of the term? At LHV, there’s no penalty for early repayment.Customer service

LHV offers clients the best service on the market. Customer satisfaction with our service and products is very important to us. Our clients feel that we understand their needs and interests and that their loan account manager is always there for them, a financial partner who can be trusted.Other products and services, online banking and mobile app

A responsive and user-friendly mobile app saves your time. People value convenience and being able to get their banking done in a location-independent manner – from home, work or abroad.

What’s the next step toward becoming a homeowner?

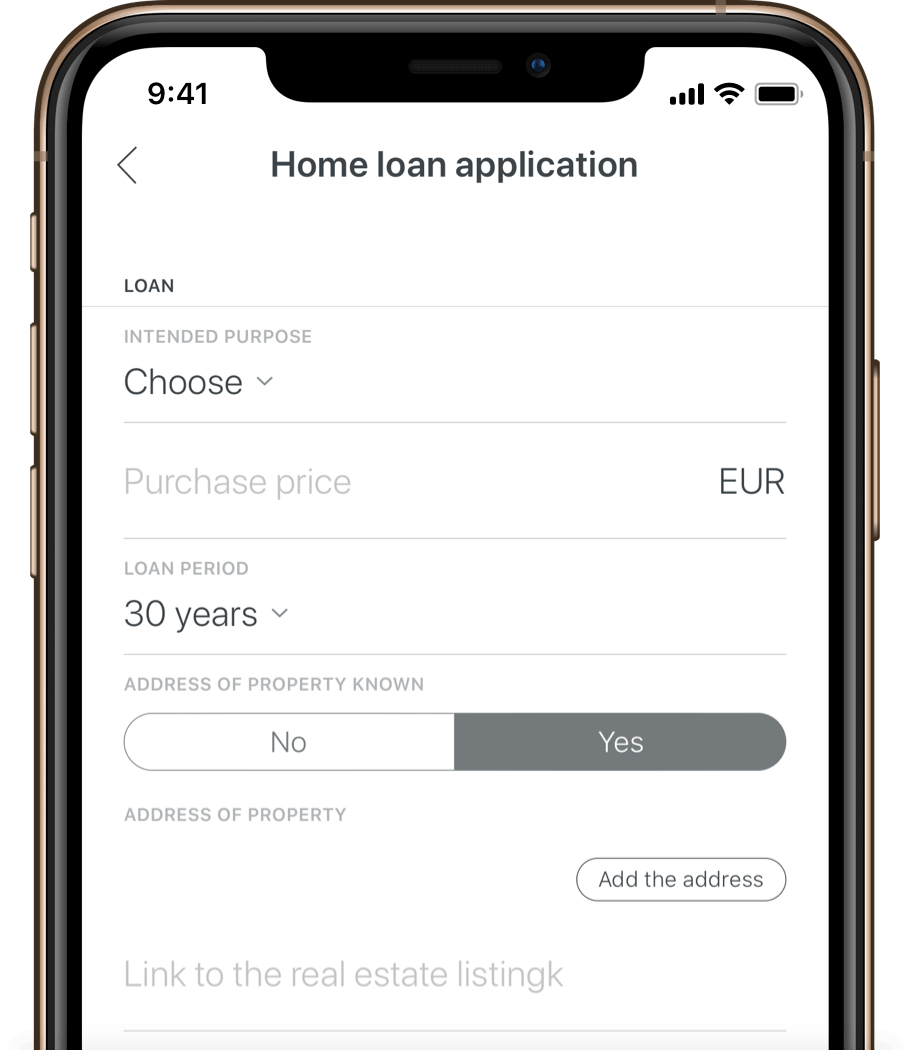

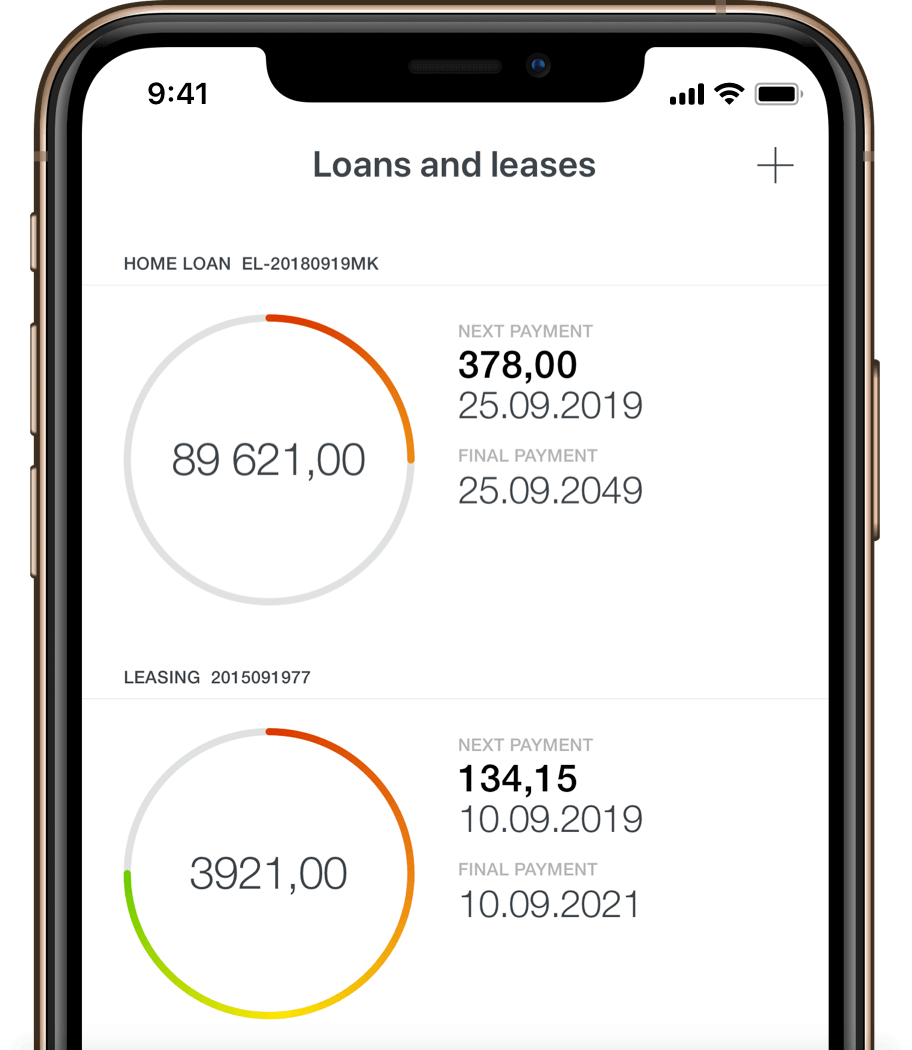

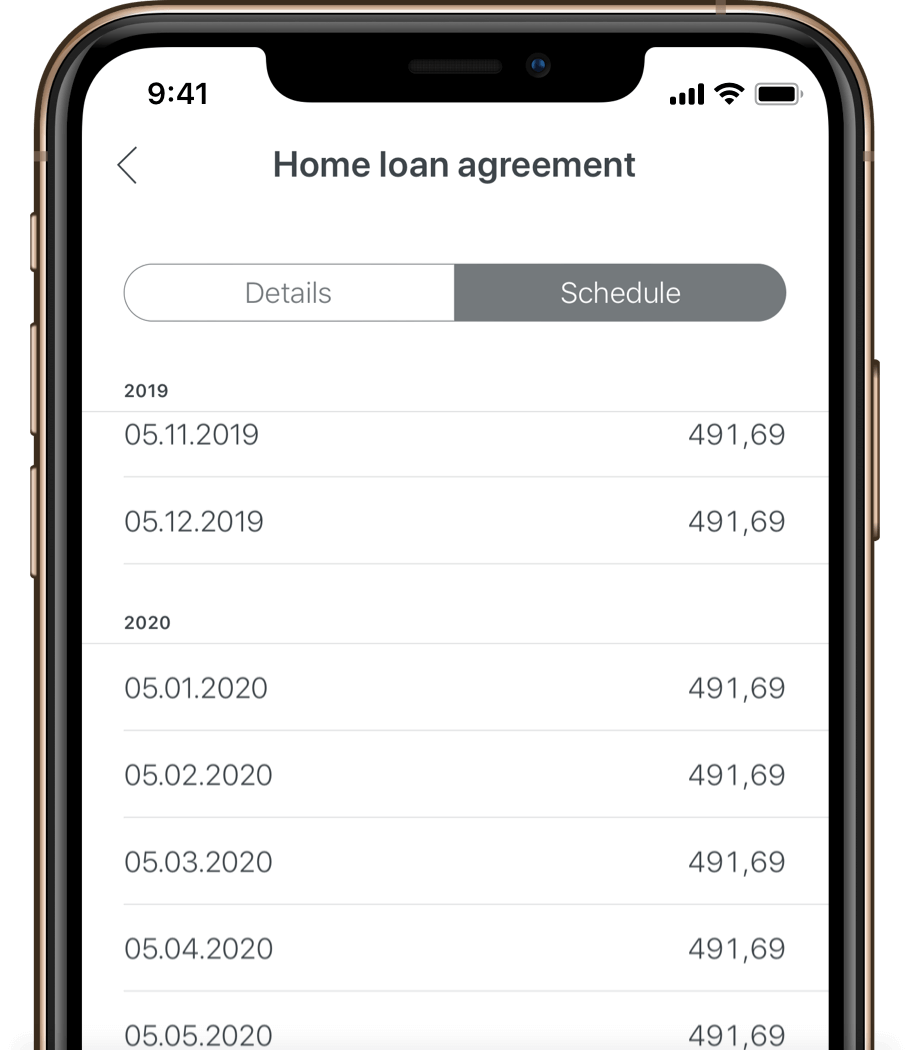

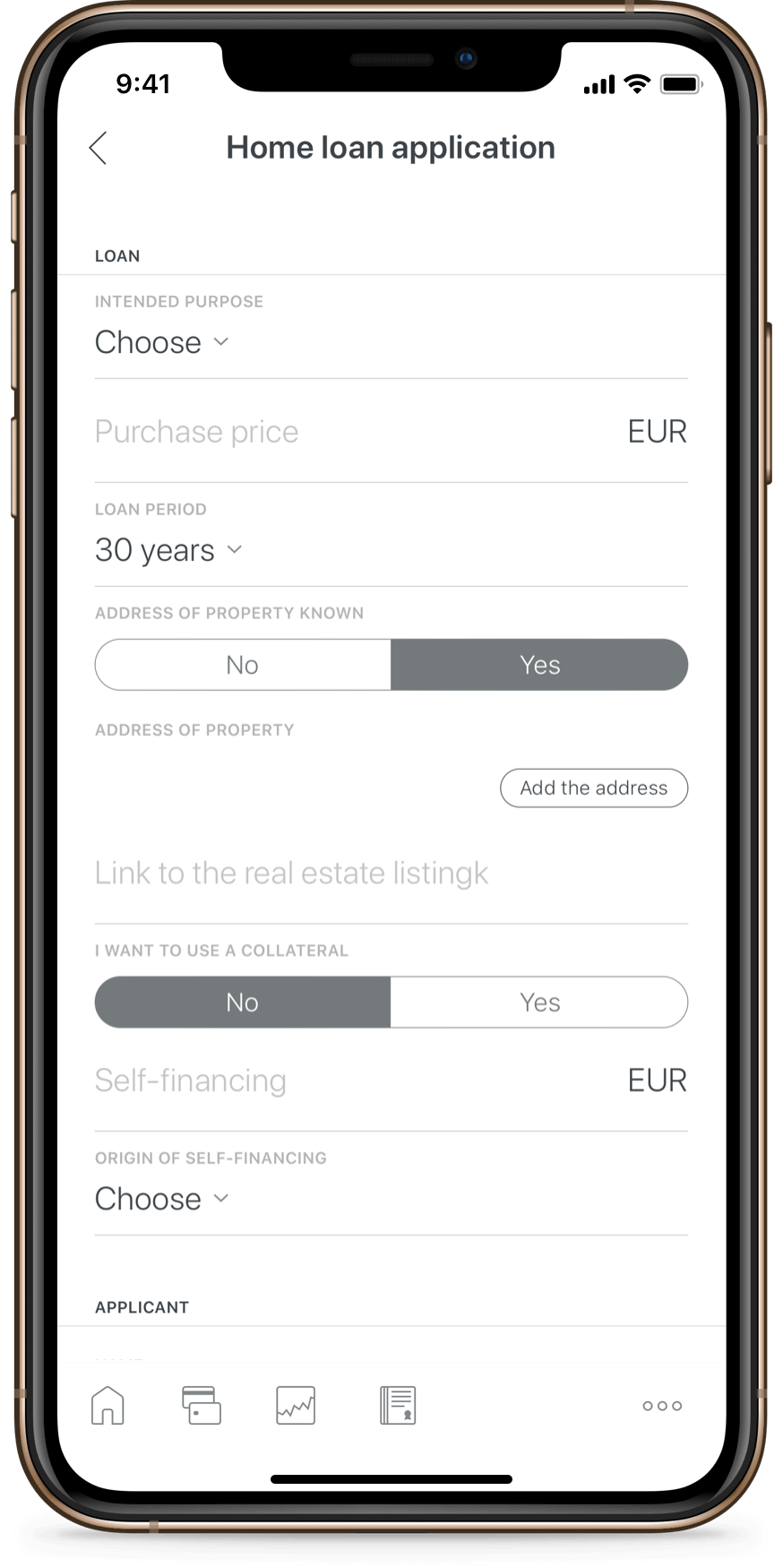

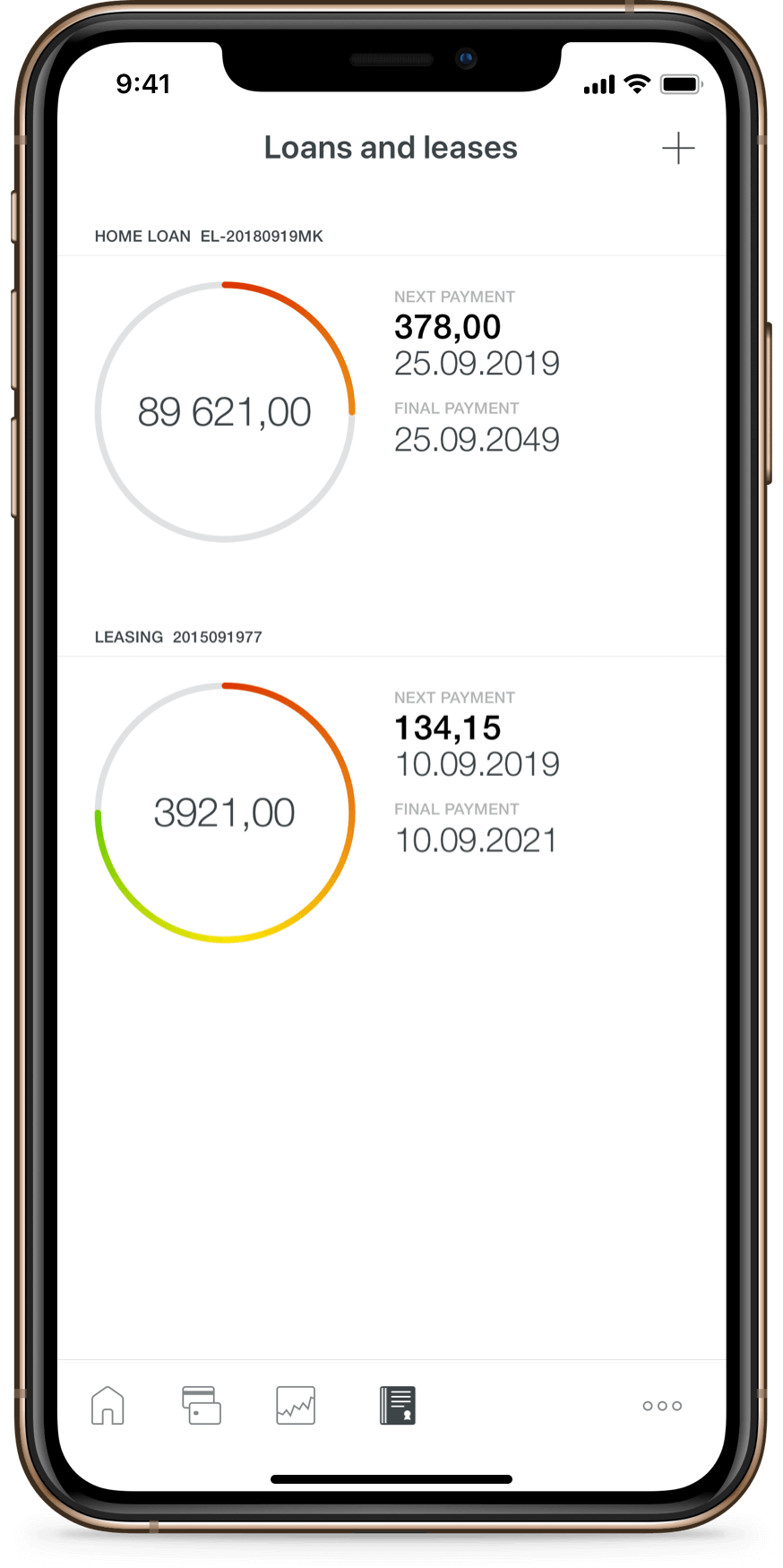

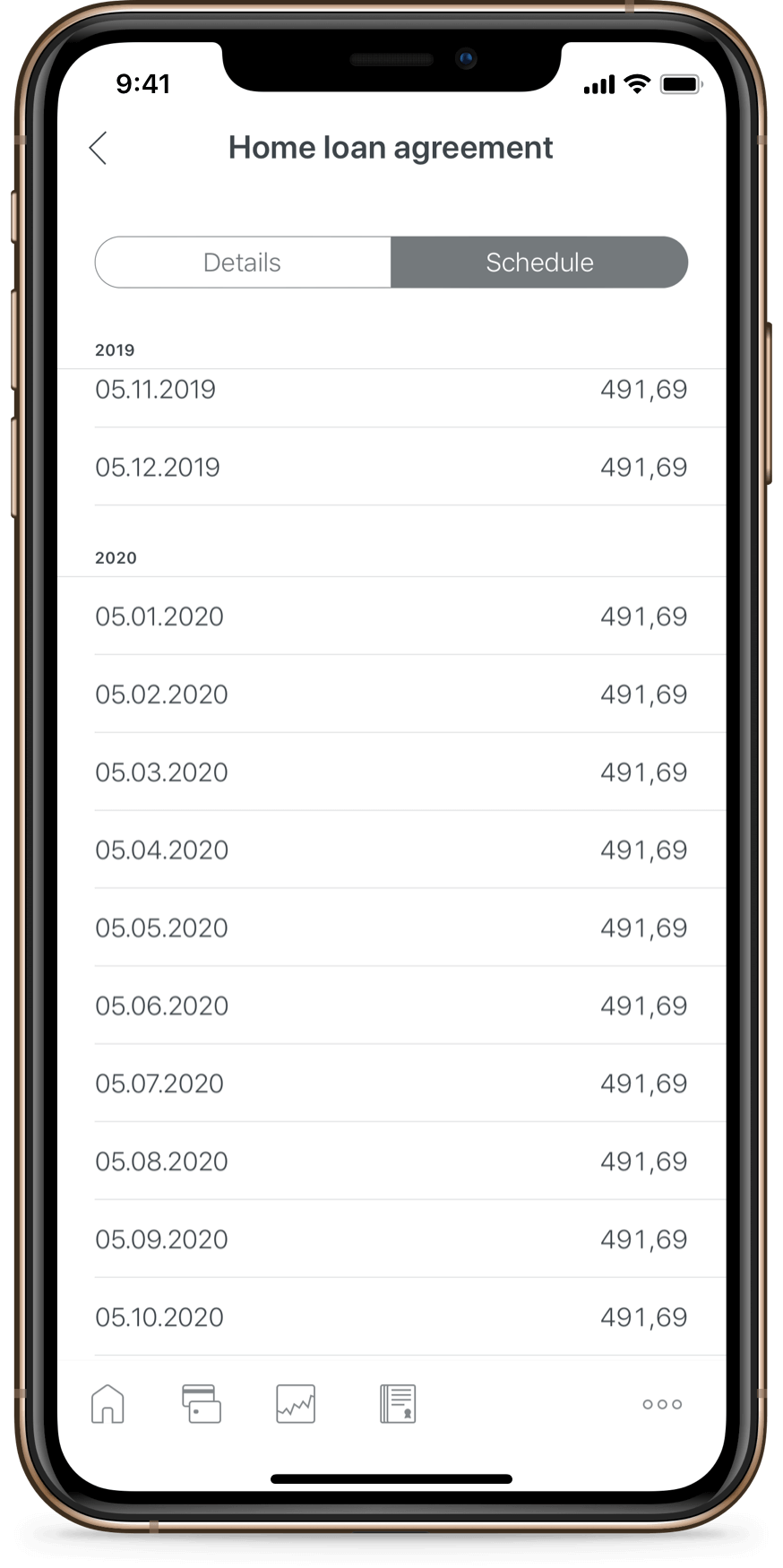

Download LHV mobile app to

apply for a home loan

view your loan balance and next payments information

view your payment schedule

Customer support

Call 699 9119 from 9-17 on weekdays or email kodulaen@lhv.ee